Net Worth vs Annual Income: The Difference Most People Get Wrong

What's the difference between net worth vs annual income?

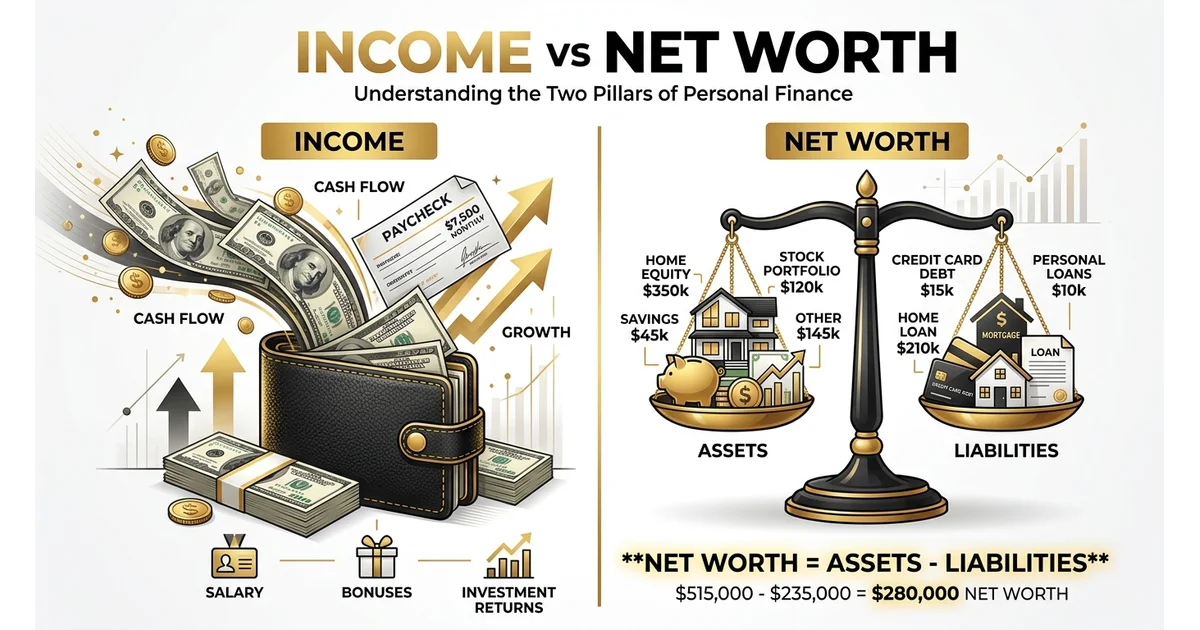

Annual income is the money you earn in a given year — your salary, business profit, or investment returns. Net worth is what you actually own minus what you owe, measured at a single point in time. A person can earn a high income and still have a low (or negative) net worth if they spend it all or carry heavy debt. A person can also earn a modest income and have a high net worth if they’ve saved and invested consistently over time.

Quick Comparison

| Income | Net Worth | |

|---|---|---|

| What it measures | Money earned over a period (monthly/yearly) | What you own minus what you owe, at one moment |

| Type of measurement | A “flow” — ongoing | A “snapshot” — fixed point in time |

| Can it be negative? | No (though take-home pay after debt payments can feel that way) | Yes, if debts exceed assets |

| Example | “$90,000 a year” | “$25,000 total” |

The Core Definitions

Income is money you receive on a regular, recurring basis — typically through a job, a business, or investments. It’s measured over a period of time: per month, per year. Your salary is income. Freelance payments are income. Dividends from stocks are income.

Net worth is calculated differently: total assets minus total liabilities, at a specific point in time. Assets are things you own with monetary value — cash, real estate, investments, a car. Liabilities are what you owe — mortgages, car loans, credit card debt, student loans. Once you total your assets and subtract your liabilities, the result is your net worth. If liabilities are greater than assets, the result is a negative net worth.

Why You Can Earn a Lot and Still Have Low Net Worth

This is the part that surprises people. A useful real example, imagine a friend who earns $100,000 a year but carries enough debt that their net worth is only $15,000. Meanwhile, you earn $70,000 a year, but a decade of consistent investing has brought your net worth to $100,000. Despite earning less annually, you’re meaningfully wealthier by net worth — the metric that actually reflects financial stability.

Maclear’s blog frames this with two illustrative examples. One person earns $180,000 a year but spends nearly all of it on a luxury apartment, a new car payment, and frequent dining out — leaving a net worth close to zero, or even negative once debts are counted. Another person earns $70,000 a year, lives more modestly with roommates, and saves consistently — ending up with a net worth over $60,000 and growing. The person earning less than half as much is, by the only metric that matters for long-term financial security, ahead.

This pattern even has a name in personal finance circles: HENRYs — “High Earners, Not Rich Yet.” These are people with strong incomes who haven’t converted that income into lasting assets, often because of lifestyle spending that scales up alongside their paycheck.

Why This Confusion Is Everywhere in Celebrity Net Worth Coverage

This distinction matters far beyond personal budgeting — it’s also one of the most common errors in how celebrity and athlete wealth gets reported. A frequent mistake looks like this: an athlete signs a $20 million contract, and a website immediately reports that the athlete now “has a $20 million net worth.” But a signed contract value isn’t net worth at all — it’s future income, and even then, taxes, agent fees, and living expenses will reduce how much of that $20 million actually becomes savings or assets. The athlete’s real net worth depends on what happens to that money after it’s earned, not the headline figure of the deal itself.

This is exactly the kind of conflation that produces wildly different “net worth” estimates for the same public figure across different websites — one site may be citing total career earnings, another may be citing a single year’s contract value, and a third may be making an actual attempt at assets-minus-liabilities. None of these are interchangeable, even though they often get presented as if they are.

For a deeper look at how this plays out specifically in sports contracts, see Athlete Contracts Explained — and for a real example, Anthony Edwards net worth profile shows exactly how a single contract gets reported at several different total values depending on what’s actually being measured.

How to Calculate Your Own Net Worth

The process is straightforward:

- List your assets — cash and savings, retirement accounts, investments, real estate, vehicles, and other items of significant value

- List your liabilities — mortgage balance, car loans, credit card debt, student loans, any other money owed

- Subtract liabilities from assets — the result is your net worth

If you own a home worth $300,000 and still owe $100,000 on the mortgage, that home contributes $200,000 to your net worth — not $300,000.

A Quick Note on Gross vs. Net Income

Since “net” shows up in both terms, it’s worth clarifying one more related pair. Gross income is your total earnings before taxes and deductions — the big number at the top of a pay stub. Net income is what’s left after taxes and deductions are removed — the number that actually lands in your bank account. Confusing gross and net income is a separate (but related) mistake from confusing income with net worth — both lead to overestimating how much money someone actually has available.

Which One Actually Matters More?

Most financial educators land in the same place on this. As Yahoo Finance’s Sarah C. Brady puts it, income is important — it’s the fuel that builds net worth — but it isn’t itself a measure of financial health. Two people with identical six-figure incomes can be in completely different financial positions depending on what they do with that money. Net worth, because it accounts for both what’s been earned and what’s been kept (versus spent or owed), is the more reliable long-term indicator of actual wealth.

Frequently Asked Questions

What is the simplest definition of net worth?

Net worth is everything you own (assets) minus everything you owe (liabilities), calculated at a specific point in time.

Can someone have a high income but low net worth?

Yes, and it’s common. This happens when spending and debt grow alongside income — sometimes called “lifestyle inflation.” A high earner with significant debt and little savings can have a lower net worth than a moderate earner who saves consistently.

Is a $1 million salary the same as being a millionaire?

No. A millionaire is technically someone with a net worth of $1 million or more — not someone who earns $1 million in a year. Someone earning $1 million annually with heavy spending and debt might have a net worth far below $1 million.

Why do celebrity net worth estimates vary so much between websites?

Often because sites conflate different metrics — total career earnings, a single contract’s value, or actual assets-minus-liabilities — without clarifying which one they’re citing. A signed contract is future income, not current net worth.

How often should I calculate my net worth?

Most financial guides suggest monthly, quarterly, or at least annually, depending on how closely you want to track your financial progress over time.

What counts as a liability when calculating net worth?

Any money owed: mortgage balances, car loans, credit card debt, student loans, and other outstanding financial obligations.

Conclusion

Income and net worth answer two different questions: income asks “how much are you earning right now,” while net worth asks “how much have you actually kept.” They’re related — income is the primary tool most people use to build net worth — but they’re not interchangeable, and treating them as the same thing is exactly what produces the inflated, inconsistent wealth figures that show up across celebrity and athlete coverage. A signed contract, a high salary, or a big payday is income. What’s left after spending, debt, and taxes is what actually becomes net worth.